It can be difficult to know exactly when you should retire. There are a lot of questions that go into that decision:

- At what age should you retire?

- Do you know what you want to do in retirement?

- Do you know what retirement lifestyle you want?

- How much do you have in your retirement savings?

- How long will that savings last?

- How do Social Security payments impact your retirement?

And so many more considerations.

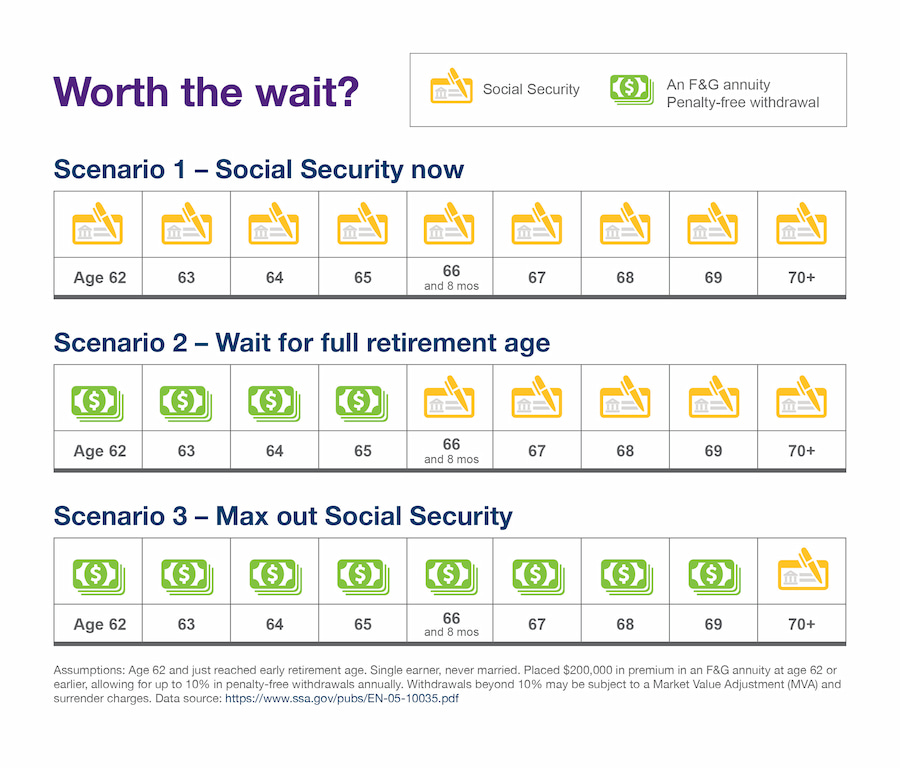

Answers to these questions will depend on your personal needs and preferences. Be sure to talk through your options with your financial professional. Depending on your situation, you might choose to retire as soon as you’re eligible for Social Security or you might wait to maximize your payments. If you choose the latter, an annuity could help you maximize those payments. Let’s look at how.

How an annuity can help

According to the Social Security Administration, “full retirement age is 66 if you were born from 1943 to 1954, and it increases gradually if you were born from 1955 to 1960. Anyone born in 1960 or later, full retirement benefits are payable at age 67.”

Have you and your agent considered the impacts of delaying your Social Security1 income? The results may vary based on how old you will be when you retire.

If you want to retire on your own schedule, an annuity may be one option to help make that possible, while making the most of your hard-earned Social Security income.

Annuities offer penalty-free withdrawal of a portion of your retirement nest egg each year. If you’re able to live off of this income, you could delay starting Social Security until you reach full retirement age and avoid a payment reduction. Wait a few years more, and you can enhance your annual Social Security payout even further.

Your remaining annuity balance when you reach your Social Security goal can continue to grow or be converted into a supplemental income stream you can’t outlive.

1 If you delay receiving Social Security benefits until after your full retirement age, your monthly benefit continues to increase.

When you reach age 70, your monthly benefit stops increasing even if you continue to delay taking benefits.

How the Social Security math works out

Let’s assume you just turned 62 years old. That makes you eligible for early retirement, according to the Social Security Administration.

Start Social Security now, and you’ll sacrifice 28.3% of every Social Security check as long as you live.

Wait until full retirement age,2 and get that much more for life. Plus, you could earn yourself approximately 8% more each year beyond full retirement age that you wait, up to age 70.

2 Full retirement varies based on when you were born. Until 1954, it’s 66 years old. Born from 1955 to 1964, it increases in two-month increments until reaching 67.

Visit SSA.gov for details on your specific situation.

Evaluate your Social Security situation

Each person’s situation can look different. Your birthdate, marital status and what you’ve contributed to Social Security can impact your payment amount. The Social Security Administration offers a handy calculator to determine your full retirement age and the impacts to retiring at various ages.

If you’re interested in learning more about how Social Security affects your individual retirement needs, contact a financial professional today.

/Hubspot_FG%20Logo%20Name%20Purple%20Bkgd.svg "Hubspot_FG Logo Name Purple Bkgd")